Money is stressful. We all know the feeling. Tracking every single dollar feels like a full-time job. That is precisely why money management software development is exploding right now. People want a single, clean place to see their income, bills, and savings. They want a tool that makes them smarter with their cash. In this guide, I’ll show you exactly how to develop money management software that users will actually love.

Quicken-like software development remains the gold standard in 2026. Why? Because Quicken built deep trust over decades. It offers powerful budgeting and detailed reports. But the market is shifting. New fintech apps are entering the scene every single day. Users now want more than just a digital ledger. They want a SaaS finance platform that thinks for them. If you are a founder or a fintech software development company, now is the time to act. Digital banking is the new normal. The demand for Money Management Software Like Quicken in 2026 has never been higher.

What Is Money Management Software?

At its heart, this software is a digital brain for your wallet. It helps users track every cent they earn and spend. Think of it as a GPS for your financial life. Personal finance software development focuses on solving real-world problems. Many people struggle with tracking daily expenses. They have poor habits and no clear plan. This software fixes that. It provides total visibility into cash flow.

When you build money management software like Quicken, you solve the “where did my money go?” mystery. Popular tools like Mint and YNAB have paved the way. They show that users value simplicity. They want to see their net worth on a clean, beautiful dashboard. They want personal budgeting tools that work on their phones, tablets, and desktops. By focusing on these pain points, your money management app development project will have a rock-solid foundation.

Why Build a Money Management App in 2026?

The timing is perfect for a few big reasons. Digital banking users are at an all-time high. Everyone has a smartphone, and everyone wants to save money. There is a massive hunger for an AI-powered finance app. People don’t just want data; they want insights. They want an app that says, “Hey, you spent too much on coffee this week, maybe skip the latte tomorrow.” This shift toward intelligence is a massive opportunity for personal finance app development.

Business-wise, the numbers look great too. The subscription-based model is a gold mine for revenue. Users stay loyal to their finance apps because moving years of data is a significant hassle. This leads to incredibly high customer retention. If you offer a subscription-based finance app, you get steady, recurring revenue every month. It is a scalable model that grows as you add more features. The market for money management software, like Quicken, in 2026 is ripe for innovation.

Benefits of Money Management Software Like Quicken

Why do people flock to these apps? The benefits are clear for both the people using the app and the companies building it.

Benefits for Users

Total Financial Control: Users see precisely where their money is at any moment.

Effortless Tracking: Automated tools eliminate manual receipt entry.

Real-Time Data: Instant updates from banks provide a live view of net worth.

Smart Goal Setting: Users can plan for a house, a car, or a vacation with clear timelines.

Lower Stress: Having a plan reduces the “end of the month” panic.

Better Habits: The app coaches users to spend less and save more.

Benefits for Businesses

Steady Revenue: Monthly or yearly subscriptions create a predictable income stream.

Deep User Loyalty: Once a user sets up their accounts, they rarely switch to a competitor.

Valuable Data: You can see spending trends to inform future feature improvements.

Scalable Growth: Cloud infrastructure enables you to add millions of users easily.

Upsell Potential: You can offer premium tax help or investment advice.

Brand Authority: Being a trusted financial tool makes you a leader in the fintech space.

Key Features of Software Like Quicken

To compete with the big players, you need a mix of core basics and futuristic “wow” features. Here is what you should include in your money management software development plan.

Core Features

Secure User Onboarding: A fast, safe way to create an account and verify identity.

Automated Expense Categorisation: The app should know “Starbucks” is “Food” without being told.

Bank Account Syncing: Real-time links to checking, savings, and credit card accounts.

Flexible Budget Creation: Tools for zero-based, 50/30/20, or custom budget styles.

Bill Reminders: Push notifications that ensure no one ever pays a late fee again.

Visual Dashboards: Clean charts and graphs that show spending at a glance.

Searchable History: The ability to find a specific transaction from three years ago in seconds.

Advanced Features (2026 Trends)

AI Financial Insights: Predictive tools that warn users about upcoming cash shortages.

Investment Tracking App Tools: A dedicated space to monitor stocks, crypto, and 401 (k) s.

Voice Assistant Integration: Letting users ask their phone, “How much is in my travel fund?”

Tax Optimisation: Automatically flagging tax-deductible business expenses.

Multi-Currency Support: Essential for digital nomads and international travellers.

Shared Wallets: Features for couples or roommates to manage household bills together.

Carbon Footprint Tracking: Showing the environmental impact of certain purchases.

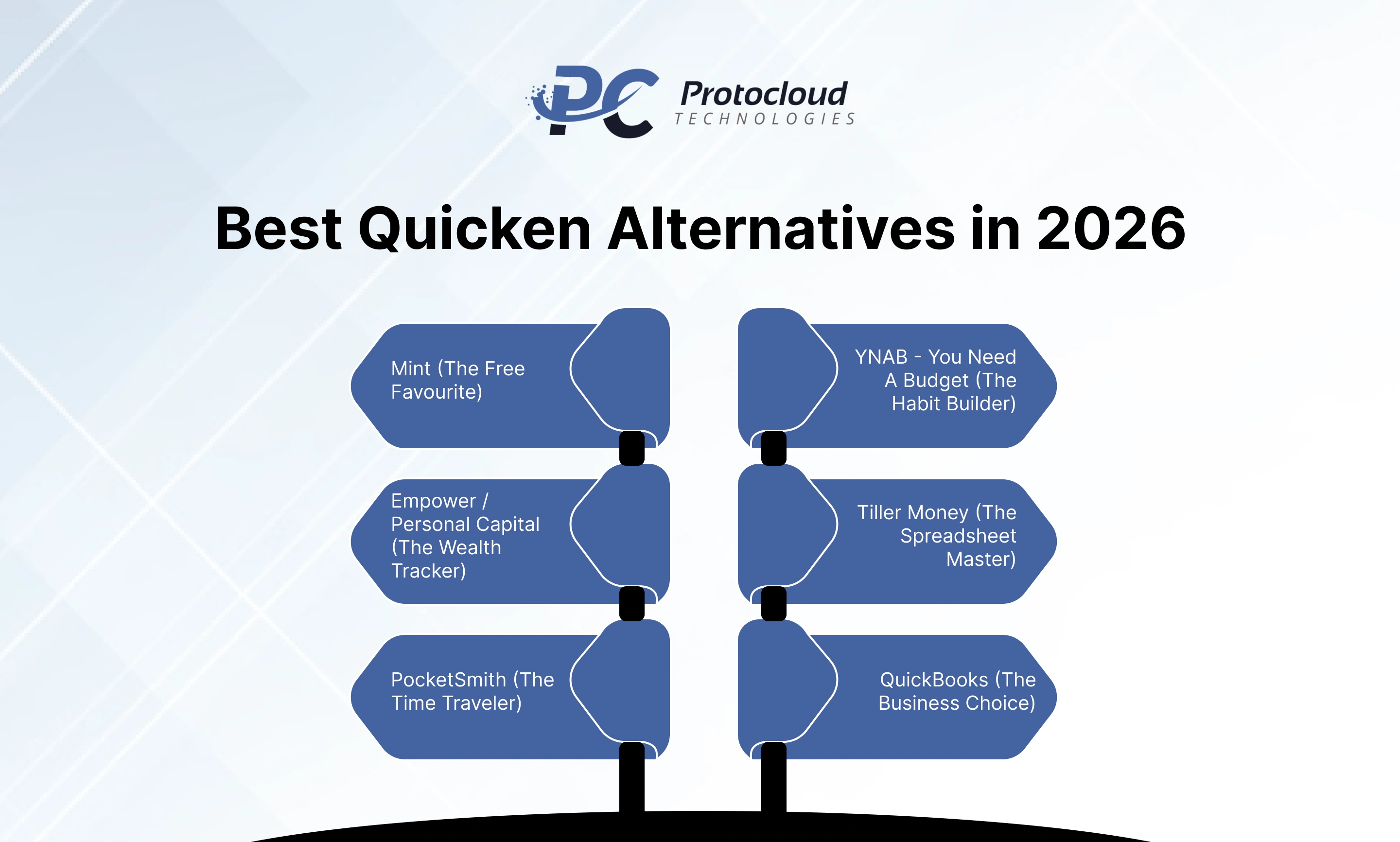

Best Quicken Alternatives in 2026

The market for Quicken alternatives in 2026 is diverse. Each app targets a specific type of person. If you want to build the next big thing, you must understand what these competitors offer and where they fall short.

1. Mint (The Free Favourite)

Mint is the most famous name in the game. It is a great Mint alternative for beginners. It is free to use because they make money through ads and referrals. It offers a spotless interface and basic automated expense categorisation. However, many power users find it too simple for complex needs.

2. YNAB – You Need A Budget (The Habit Builder)

YNAB is the king of “giving every dollar a job.” It is the best YNAB alternative for people who are serious about getting out of debt. It uses a zero-based budgeting system. Users love it because it changes how they think about money. The downside? It has a steep learning curve that can scare away casual users.

3. Empower / Personal Capital (The Wealth Tracker)

If you care more about your “big picture” net worth than your daily coffee spend, this is the one. It is a top-tier investment tracking app. It shows you how your stocks and retirement accounts are doing. It is perfect for high-income earners but lacks the deep, granular budgeting tools found in other apps.

4. Tiller Money (The Spreadsheet Master)

Tiller is a unique Tiller Money alternative. It automatically pulls bank data into Google Sheets or Excel. It is perfect for “data nerds” who want total control over their numbers. You can build your own formulas and charts. However, it is not as mobile-friendly as a dedicated app.

5. PocketSmith (The Time Traveler)

PocketSmith is excellent because it focuses on the future. It lets you “forecast” your bank balance months or years in advance. It is perfect for people with complex lives or multiple properties. It is a potent financial planning software, but the price can be high for the average user.

6. QuickBooks (The Business Choice)

While primarily for companies, it is a common QuickBooks alternative for freelancers. It handles invoices and taxes perfectly. If your app targets the “solopreneur” market, you will be competing directly with this giant.

Technology Stack Required to Build Quicken-Like Software

Building a secure fintech application requires a modern, fast, and safe tech stack. You cannot afford to use outdated tools when dealing with people’s life savings.

Frontend (The Face): Use React for the web and Flutter or React Native for mobile. These provide a smooth, app-like experience across all devices.

Backend (The Brain): Node.js or Python (Django/FastAPI) is excellent. They handle high-speed calculations and massive data sets with ease.

Database (The Memory): PostgreSQL is the standard for financial data. It is reliable and keeps data structured perfectly. Use MongoDB for handling unstructured analytics.

Banking APIs: This is the most crucial part. You need Plaid, Yodlee, or Salt Edge to connect to thousands of banks globally.

Cloud Infrastructure: Use AWS (Amazon Web Services) or Google Cloud. They offer the best security and can scale as you get more users.

Step-by-Step Process to Develop Money Management Software

Developing a finance app is a marathon, not a sprint. You need a clear plan to turn an idea into a finished product.

Market Research: Look for gaps in the current Quicken alternatives. What are users complaining about in the App Store?

Define Your MVP: Pick the 3-5 essential features. Don’t try to serve everyone on day one.

UI/UX Design: Create a “low-stress” design. Money is scary, so use a clean layout and friendly colours.

Backend & API Setup: Create the engine that powers your data smoothly and securely. Connect your banking API integration early to test data flow.

Develop Core Logic: Write the code that categorises expenses and calculates budget totals.

Security Implementation: Add end-to-end encryption and multi-factor authentication. This is non-negotiable.

Quality Assurance (QA): Test the app with real data. Make sure every cent is accounted for. Financial bugs are the worst kind of bugs.

Beta Launch: Release the app to a small group of users. Get their feedback and fix any friction points.

Full Release & Marketing: Put your app on both stores and let people start using it. Use SEO to show people how your app solves their money problems.

Post-Launch Support: Regularly update the app to fix bugs and add the next set of features from your roadmap.

Security and Compliance Requirements in 2026

In 2026, hackers are more intelligent than ever. Your financial data security must be impenetrable. If users don’t trust you, they won’t link their banks. It is that simple.

Data Encryption: Use AES-256 to encrypt stored data and TLS to secure data while it moves.

Multi-Factor Authentication (MFA): Requires a code from an app or a fingerprint to log in.

GDPR & PCI-DSS: Follow these global rules for handling personal and card data.

Regular Penetration Tests: Hire ethical hackers to attempt to breach your system.

Biometric Security: Use Face ID or Touch ID for quick, secure mobile access.

Tokenisation: Never store actual bank login details; use secure “tokens” provided by APIs like Plaid.

Cost to Develop Money Management Software Like Quicken

Building a high-quality app isn’t cheap, but it is a massive investment. The cost to develop money management software depends on how “fancy” you want it to be.

Simple MVP: This might cost between $40,000 and $70,000. It covers basic tracking and a single platform (e.g., iOS).

Full-Scale App: A product with AI, investment tracking, and cross-platform support can range from $100,000 to $250,000+.

Ongoing Costs: Remember to budget for server fees, API costs (which may be per-user), and a support team.

The biggest cost drivers are the number of integrations and the complexity of your AI-powered finance app features. To build a top-tier Money Management Software Like Quicken in 2026, you need a team that understands both finance and high-end coding.

Monetisation Models for Money Management Apps

How do you turn your code into cash? There are several ways to make a profit while still helping your users.

Monthly Subscriptions: The most common model. Users pay $5- $15 per month for the full feature set.

Freemium: Offer the basic budget for free, but charge for investment-tracking tools or business reports.

Referral Fees: If a user needs a better savings account, you can suggest a partner bank and earn a fee when they sign up.

In-App Purchases: Sell one-time “premium” report templates or financial planning guides.

White-Labeling: Sell your software to smaller banks or credit unions so they can offer it to their customers.

Challenges in Developing Financial Software

You will face hurdles. Knowing them now helps you prepare.

User Trust: It takes a long time to build and a second to lose.

Banking Connectivity: Sometimes bank APIs go down. Your app needs to handle these gaps gracefully.

Complex Regulations: Every country has its own laws governing financial data.

Data Accuracy: If your app says a user has $100, but they actually have $90, they will be depressed.

App Performance: People check their money on the go. The app must load in under two seconds.

How AI and Automation Will Shape Finance Apps in 2026

The future is “invisible.” We are moving toward a world where users don’t have to do anything. Automated expense categorisation is just the tip of the iceberg. AI will soon be able to look at a user’s habits and say, “You can afford to invest an extra $200 this month.”

Imagine an app that automatically negotiates your cable bill down. Or one that finds a better insurance rate and switches you with one tap. This is the level of AI financial insights that will define the winners in the 2026 market. By building these innovative features into your money management software plan, you ensure your app stays relevant for years to come.

Why Choose a Professional Software Development Company?

This isn’t a project for a beginner. Finance is a high-stakes world. A professional fintech software development company brings several things to the table:

Deep Security Knowledge: They know how to build a secure fintech application that passes audits.

API Experience: They have worked with Plaid and Yodlee hundreds of times.

Scalability Expertise: They know how to structure your backend so it doesn’t crash when you hit 100,000 users.

Faster Time-to-Market: They have existing frameworks that speed up the money management app development process.

Conclusion

Developing a successful Money Management Software Like Quicken in 2026 is one of the best moves you can make in the fintech space. People are more focused on their financial health than ever before. If you can provide a tool that is secure, smart, and easy to use, you will find a loyal audience.

Start with a clear focus. Build an MVP that solves one big problem perfectly. Listen to your users and add features like AI financial insights over time. Developing money management software is a journey, but with the right tech and a focus on user trust, you can build a platform that truly changes how people manage their money.

FAQs

1. How long does it take to develop money management software?

Usually, it takes 4 to 9 months to go from idea to launch. This depends on how many finance management app features you want at the start.

2. Is Quicken-like software suitable for startups?

Absolutely. Startups can move faster and build better mobile experiences than big, older companies.

3. What are the best Quicken alternatives in 2026?

Mint, YNAB, Empower, and Tiller Money are the current leaders. Each serves a different niche.

4. How secure are finance apps?

When built correctly with end-to-end encryption and MFA, they are incredibly safe—often more secure than traditional banking websites.

5. Can AI improve money management apps?

Yes. AI handles the tedious work of sorting transactions and provides “predictive” advice to help users save more.